jetcityimage

Investing in railroads may not interest everyone. However, when we find a railroad whose odds to outperform the market are good, then most of us are willing to further understand the opportunity. As a matter of fact, Norfolk Southern (NYSE:NSC) could be the best railroad in the next few years. Up until early 2022, it was the only railroad that constantly outperformed the S&P500 (SPY) together with its peer CSX Corporation (CSX). Then a bear market came, but while CSX has started trading upwards once again, Norfolk has been decoupling from its peer also because of the negative impact of the East Palestine, OH, derailment that occurred on February 3, 2023, driving $1.7 billion in extra costs related to the incident. It has only recently been found that an overheated wheel bearing on a hopper car was the cause of the whole catastrophe.

From this chart, we could already guess Norfolk should gain back some ground and move closer to its 10-year trend. But this may be too backward-looking to characterize an investment. More substantial reasons come from macroeconomic data that I would like to share.

Before we move on, let me disclose that I have often been critical of Norfolk and other railroads due to their choice of funding huge buybacks by leveraging their balance sheet. The result was an increase in debt, which caused these buybacks to stop once interest rates increased. As expected, most railroads saw downward pressure on their stock price because of this. I have explained elsewhere why I chose Canadian National (CNI) as my largest position, exactly because of its conservative management of its balance sheet.

In late 2023, I thought the stock had been punished enough once it dipped below $200, and I upgraded by rating to a buy. But after a 20% run-up and a soft Q1 2024 report, I once again turned neutral and downgraded it to a hold. Since then, the stock has underperformed the market by over 21 percentage points.

So, why am I now willing to upgrade my rating once again and consider stepping into Norfolk, and buying my first shares?

The frame is changing for Norfolk

Before we move on, we must all be aware of the specific method I use to assess railroads. In short, I have studied Warren Buffett’s investment in BNSF and from there, reverse engineered the criteria he used to gauge the quality of the deal. From this work, I came to a few metrics that are not used as much as other more traditional ones. In particular, Buffett stresses the importance of a railroad’s earning power, calculated as pretax earnings divided by interest expense. The higher the ratio, the safer the company. Of course, efficiency is key in railroading, and Buffett usually looks at fuel efficiency as an overall proxy for the whole category. Being capital-intensive businesses, railroads must be careful with their balance sheet and their use of capital. The main purpose is to reinvest it back into the business to earn a decent rate of return. This is done by maintaining and enhancing the huge properties each Class 1 railroad owns and operates. FCF should be the only source for shareholder returns via dividends and buybacks. But, if a railroad can grow its revenue and its earnings, then it can expand its balance sheet accordingly, keeping its leverage at the same level while borrowing money that, in this case, can be rightly returned to the shareholders as a way to share part of the railroad’s growth. But a railroad’s top line moves according to two drivers which may partly offset one another. A railroad’s revenue depends not only on freight, but also on the fuel surcharge program. If fuel goes up, in around 60 days a railroad can charge its customers for the extra costs. This increases a railroad’s revenue even if freight traffic, volumes, or prices are decreasing. As a result, to understand a railroad’s operations, it is better to look at ex-fuel revenues when they are available.

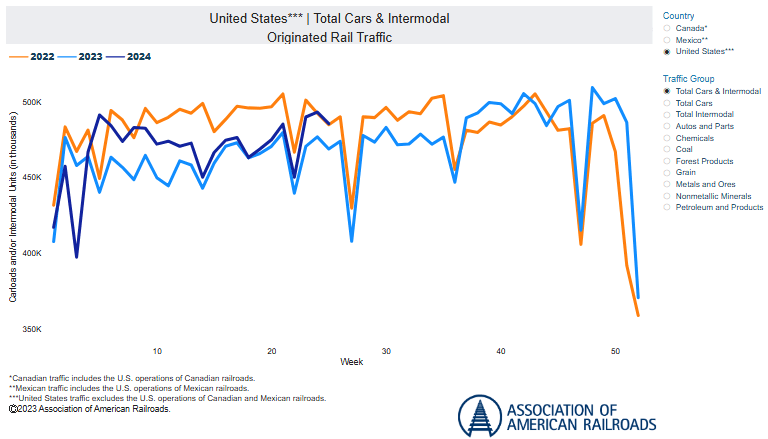

Regarding Norfolk Southern, the first good news comes from the weekly rail traffic report for June. Here, the Association of American Railroads (AAR) reported that U.S. carloads were down 1.7% in June, but up 39% considering intermodal originations. This is sensitive information for Norfolk because, on average, around 25% of its revenue comes from intermodal. True, intermodal has the lowest revenue per unit among all commodities Norfolk transports (only $754 at the end of Q1 2024 vs. $4,039 for chemicals). But capital-intensive business need volumes to cover their costs and the contribution margin coming from intermodal is therefore of great importance for the overall profitability of the company.

{kind=link}

The increase in intermodal has been going on throughout Q2. Moreover, traffic is back at 2022 levels, although pricing is lower and, as a result, revenues are too. But for freight prices to go up, demand is needed, as well as volumes. As a result, the slow but steady increase we have seen so far in the first half of the year hints a railroad recovery is on its way.

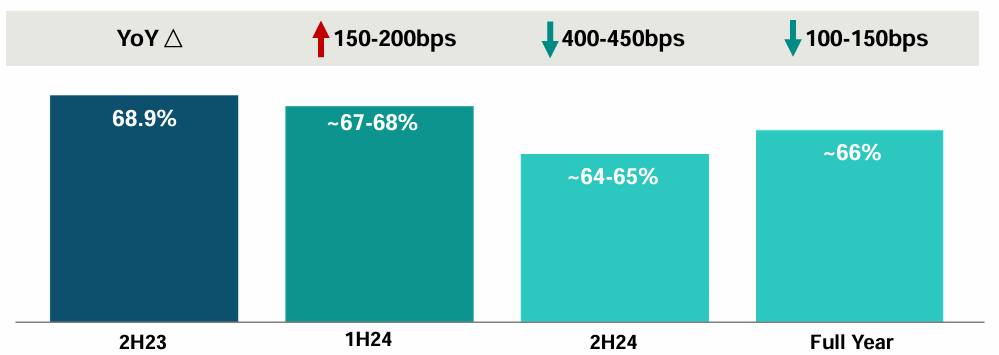

This is why Norfolk is guided by an improving operating ratio as the year unfolds. Of course, Norfolk feels the weight of the Ohio incidents and its costs, which brought its OR to above 90%. Adjusted for the incident, we are still talking about an OR closer to 70% rather than 60%. But this is the effect of decreasing volumes. When traffic and cars increase, so does the OR.

An improving OR means higher earnings and more FCF. In

NSC Q1 2024 Earnings Presentation

{kind=link}

Another bright light comes from a commodity that is usually used as a proxy to gauge the upcoming manufacturing activity: chemicals. They are essential “bricks” for multiple industries. As demand for chemicals rises, we can also expect increasing activity down the value chain, with manufacturing, agriculture, pharmaceuticals, and construction activities probably doing well. Most of the top-chemical producing states are located in the East and Norfolk, therefore, is highly exposed to their results. In June, chemicals were up 6.7% and petroleum was up 14%. Norfolk reports both categories under chemicals. Therefore, we can expect a strong quarter for this key commodity. At the same time, coal keeps going down. Although coal is important for Norfolk, its RPU is almost half of that generated by chemicals. As a result, with coal going down and chemicals increasing, the mix is going to be more favorable and Norfolk should benefit in profitability and efficiency.

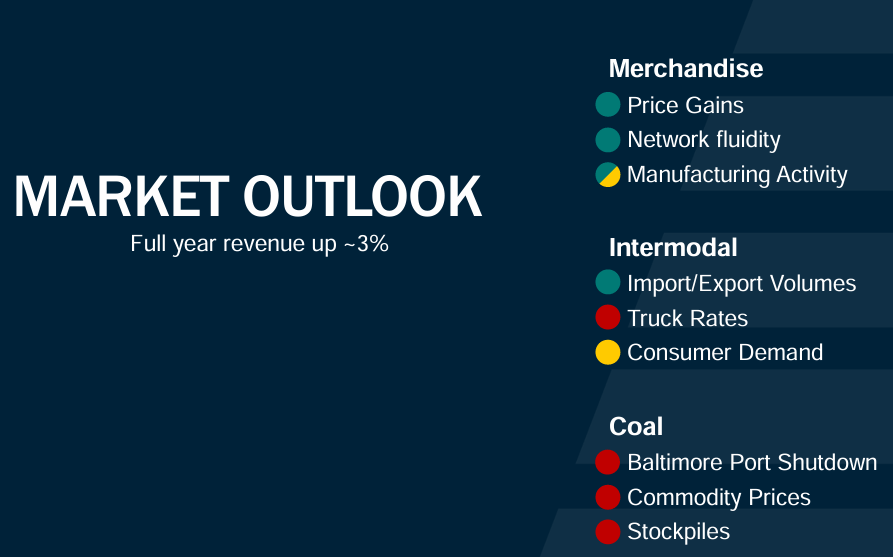

These data points are particularly important because they somehow correct Norfolk’s guidance, which is shown below. At the end of Q1, Norfolk expected merchandise to perform well and intermodal to be more or less ok.

NSC Q1 2024 Earnings Presentation

{kind=link}

But what we are seeing is a better-than-expected picture: manufacturing activity seems to have bottomed and could be picking up strength once again.

Intermodal shows increasing economic activity and demand for goods that doesn’t seem to fade.

Q2 Earnings Preview

Now, in addition to the overall picture provided by the AAR, we also have Norfolk’s weekly traffic data already available for the second quarter.

We see that chemicals’ carloads are actually down 1.2% YoY for this quarter and that petroleum is barely positive. At the same time, intermodal has increased by 76k carloads to over 1 million carloads in Q2. This will surely have an impact on Norfolk’s upcoming earnings. Motor vehicles are also doing good, but I am not too excited about these results for two reasons. On one side, we are still seeing the main automakers normalize their inventories after the hardships caused by supply chain bottlenecks and strikes. On the other hand, dealership inventories are rising, and car sales are weakening. Therefore, I expect this commodity to underperform during the second part of the year.

In any case, Norfolk is going to report 85k more carloads in Q2 vs the prior-year quarter. This is a nice 5.1% increase, which I believe will be welcomed by investors. What matters now is to understand what the average RPU may have been through the quarter. In Q1 we had an -8% YoY, which completely offset the +4% in units.

Considering a steady increase in volumes, I don’t expect pricing to be that weak, and therefore, I believe Norfolk will report positive revenue growth.

The monthly railroad fuel price index also shows declining prices, which should be favorable for railroads, which will benefit from the 60-day lag of their surcharge program, charging higher prices while spending less on fuel.

This makes me think we should see Norfolk’s net income increase more than its revenue.

Current consensus sees Norfolk report only 2.3% YoY growth. From what I gather, my expectations are higher, and I am seeing Norfolk report a 4% revenue growth to $3.1 billion. More importantly, thanks to higher volumes and lower input costs, I am expecting Norfolk’s operating leverage to produce higher EPS growth above 5%. Of course, here we will have to see the impact of the Ohio incident. We can adjust for it, but it still makes Norfolk pay a lot of cash for this disaster. But it can also create an optical distortion that makes us believe Norfolk is less profitable than what it actually is. A year ago, Norfolk reported $1.56 basic EPS. This year, as the minimum threshold, I expect it to come closer to $1.65 as a result of $372 million in net income, divided by 226 million shares outstanding. This would be a 5.8% YoY increase.

Considering the impact of the East Palestine derailment, Norfolk currently trades at an uncomfortable PE of 34. But its fwd PE is already projected to be below 22. What I believe is that Norfolk’s earnings will be higher than expected this year and could be close to $12. This would make the stock currently trade below an 18 PE ratio.

Excluding the Ohio incident, Norfolk’s operating income would have been almost $600 million in Q1 and Q2 could be well above $1 billion. On average, Norfolk spends around $500 million per quarter in capex, which means the company usually ends its fiscal year with $2 billion in FCF. This is a FCF yield of 4.1% which is decent and higher than the current 3% we see because of the derailment costs. The dividend payout ratio is 46%, but this is also affected by the sudden change in costs. Usually, Norfolk’s payout ratio is around 30% to 35%.

All in all, I am turning bullish on Norfolk once again. I see the worst is behind it, and the outlook seems improving and promising. Moreover, the effect of the derailment costs, though they weigh on the current financials, has changed many of the numbers we use to calculate the main metrics. As a result, it seems to me that Norfolk’s true multiples are lower than they appear now, and this creates an interesting opportunity for investors willing to wait until the clouds clear and the sun shines again on this company.